Relative Volume Table with PressureDisplay relative Volume as a table in the top right corner. Turns green when volume is high and price is increasing and red when volume is high and price is decreasing. I use this on D timeframe at the open to screen for stocks breaking out.

在脚本中搜索" TABLE "

ATM & ITM Strike Table (NIFTY & BANKNIFTY)This script is like a cheat sheet for option traders.

When you put it on your chart, it shows you a small table with:

The current spot price (the real market price).

The futures price (another version of the same index that sometimes trades a bit higher or lower).

The ATM strike (the strike price closest to the market price).

Which call option and put option are “in the money” and most relevant right now.

A little note to remind you if you’re looking at the right chart.

In short:

It saves you from doing mental math every time by automatically pointing out the key option strike prices you should be aware of.

Stocks Sessions TableThe stock market open session table is a great way to keep an eye on the market's open and close. This is aimed at the UK traders working with the BST timezone

Strategy Sheet — Customizable 4x8 Table📖 Script Description

The Strategy Sheet — 4 Columns / 8 Rows is a compact and highly customizable table-based tool for traders who want to keep their trading plan, rules, and session settings directly visible on the chart.

🔹 Features:

• Up to 4 fully configurable columns and 8 rows

• Compact UI with per-column color overrides

• Dark / Light / Custom theme modes

• Support for zebra row backgrounds (alternating colors)

• Adjustable position, padding, spacing, and alignment

• Clean layout with borders and header styling

• Perfect for trade plans, ORB setups, session notes, or risk rules

🔹 Use cases:

• Documenting strategy rules directly on chart

• Displaying ORB session times and risk management

• Creating a structured overview of trading setups

• Quick reference without leaving the chart

This script does not generate signals – it’s a visual aid designed to organize and display trading information in a clear and professional way.

Daily Seasonality Strength + Prediction TableDaily Seasonality Strength + Prediction Table

Return Estimates:

This indicator uses historical price data to calculate average returns for each day (of the week or month) and uses these to predict the next day’s return.

Seasonality Strength:

It measures seasonality strength by comparing predicted returns with actual returns, using the inverse of MSE (higher values mean stronger seasonality).

supports up to 10 assets

This script is for informational and educational purposes only. It does not constitute financial, investment, or trading advice. I am not a financial advisor. Any decisions you make based on this indicator are your own responsibility. Always do your own research and consult with a qualified financial professional before making any investment decisions.

Past performance is no guarantee of future results. The value of the instruments may fluctuate and is not guaranteed

U Table • LITEA compact, educational version of my workflow that combines trend, momentum, trend strength, and a clean trigger:

Trend: EMA Fast vs EMA Slow (auto-lengths by chart TF)

Momentum: RSI > 50 for longs / < 50 for shorts

Strength: ADX above a user-set threshold (fallback implementation; can be replaced by ta.adx() when available)

Trigger: price crosses the Bollinger basis (center line)

Signals

LONG: crossover(close, BB basis) while EMA Fast > EMA Slow, RSI > 50, ADX > threshold

SHORT: crossunder(close, BB basis) while EMA Fast < EMA Slow, RSI < 50, ADX > threshold

Visuals

EMA Fast / EMA Slow / BB basis

Markers “L” / “S” on triggers

Latest confirmed pivot high/low (broken line style)

Small diagnostics table (ADX, EMA relation, RSI, last pivots) on the last bar

Inputs

Pivot length: pivot confirmation window (default 5)

ADX threshold: minimum trend strength to allow signals (default 20)

Notes

Signals are intended to be evaluated on bar close. Intrabar values may change until the bar closes.

Pivot lines appear after confirmation; they do not repaint once confirmed.

No external data or security() calls are used.

This LITE build focuses on clarity and speed (few calculations, overlay-friendly). It can be used as a stand-alone study or as a scaffold for your own research and risk management.

Financial Change % Table - ToluFinancial Change % Table which includes revenue , operating profit and earning per share . compares the financial data with previous quarter QoQ and previous year YoY . and shows the change in %.

Position Sizing Risk TablePosition Sizing Risk Table - swing trading. Allowing for a 0,25; 0,5 and 1% risk based on NAV

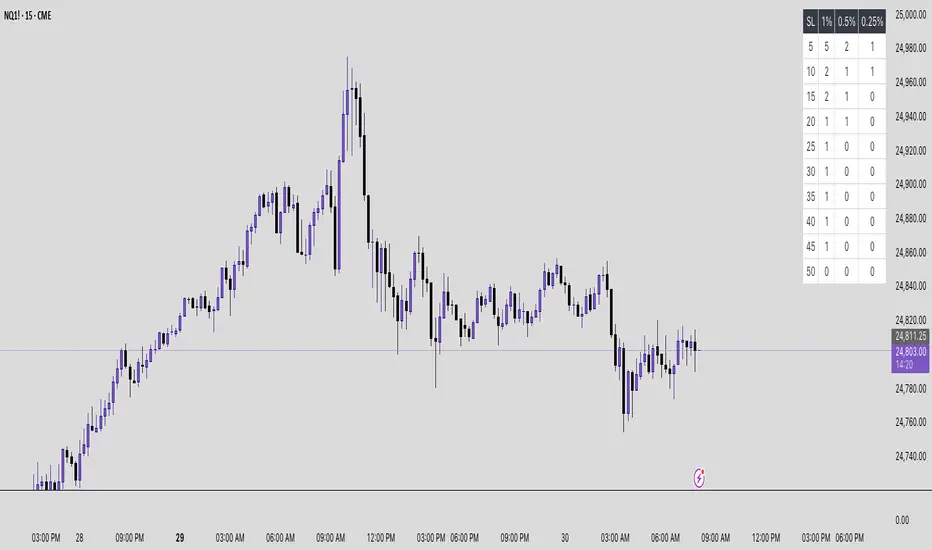

Futures Risk Contract TableFutures risk table for NQ MNQ YM MYM ES and MES

changeable capital and risk percentage along with points.

Market Sentiment - VIX Table Live RefreshProvides Market sentiment visual representation for easy understanding - using CBOE:VIX values

The VIX Sentiment Table provides an at-a-glance assessment of market mood by visualizing live data from the CBOE Volatility Index (VIX). Updated in sync with your chart’s resolution, this intuitive tool breaks down the current VIX level into clear sentiment zones—ranging from “Complacency” to “Panic”—paired with concise interpretations to guide your trading decisions.

EMA Ribbon with TableThis indicator plots multiple EMAs (5, 8, 13, 21, 34, 55, 89, 144, 233, 377) based on Fibonacci levels. Each line has a distinct color, and a clean table displays their real-time values. Great for spotting trend direction, crossovers, and momentum at a glance.

Price × Volume TableIt creates a table showing:

1- Daily Close × Daily Volume

2- Current Close × Current Volume

3- Close × Highest Volume (last 360 candles)

Yearly Performance Table with CAGROverview

This Pine Script indicator provides a clear table displaying the annual performance of an asset, along with two different average metrics: the arithmetic mean and the geometric mean (CAGR).

Core Features

Annual Performance Calculation:

Automatically detects the first trading day of each calendar year.

Calculates the percentage return for each full calendar year.

Based on closing prices from the first to the last trading day of the respective year.

Flexible Display:

Adjustable Period: Displays data for 1-50 years (default: 10 years).

Daily Timeframe Only: Functions exclusively on daily charts.

Automatic Update: Always shows the latest available years.

Two Average Metrics:

AVG (Arithmetic Mean)

A simple average of all annual returns. (Formula: (R₁ + R₂ + ... + Rₙ) ÷ n)

Important: Can be misleading in the presence of volatile returns.

GEO (Geometric Mean / CAGR)

Compound Annual Growth Rate. (Formula: ^(1/n) - 1)

Represents the true average annual growth rate.

Fully accounts for the compounding effect.

Limitations

Daily Charts Only: Does not work on intraday or weekly/monthly timeframes.

Calendar Year Basis: Calculations are based on calendar years, not rolling 12-month periods.

Historical Data: Dependent on the availability of historical data from the broker/data provider.

Interpretation of Results

CAGR as Benchmark: The geometric mean is more suitable for performance comparisons.

Annual Patterns: Individual year figures can reveal seasonal or cyclical trends.

Symbol vs Benchmark Performance & Volatility TableThis tool puts the current symbol’s performance and volatility side-by-side with any benchmark —NASDAQ, S&P 500, NIFTY or a custom index of your choice.

A quick glance shows whether the stock is outperforming, lagging, or just moving with the market.

⸻

Features

• ✅ Returns over 1W, 1M, 3M, 6M, 12M

• 🔄 Benchmark comparison with optional difference row

• ⚡ Volatility snapshot (20D, 60D, or 252D)

• 🎛️ Fully customizable:

• Show/hide rows and timeframes

• Switch between default or custom benchmarks

• Pick position, size, and colors

Built to answer a simple, everyday question — “How’s this really doing compared to the broader market?”

Thanks to @BeeHolder, whose performance table originally inspired this.

Hope it makes your analysis a little easier and quicker.

Abusuhil Bullish Candles (Label + Table)Abusuhil Bullish Candles is a pattern recognition indicator designed to identify key bullish reversal candlestick formations including Hammer, Bullish Engulfing, Morning Star, Piercing Line, Three White Soldiers, and Three Inside Up.

The script includes optional filters such as Stochastic and Volume Confirmation, providing more precise signal detection.

Each pattern and filter is fully customizable via settings. Alerts are also included to support active trading workflows.

This script was written originally and does not copy open-source indicators. It's ideal for traders seeking visual clarity on bullish opportunities with professional-grade logic.

مؤشر الشموع الصعودية هو مؤشر احترافي يكتشف أبرز نماذج الانعكاس الصعودي في الشموع اليابانية مثل: Hammer، Bullish Engulfing، Morning Star، Piercing Line، Three White Soldiers، و Three Inside Up.

يوفر المؤشر فلاتر إضافية مثل فلتر Stochastic وفلتر الفوليوم لتعزيز دقة الإشارات. جميع الإعدادات قابلة للتعديل بما يتناسب مع احتياج كل متداول.

يحتوي المؤشر أيضًا على تنبيهات تلقائية لدعم استراتيجيات التداول اللحظي. تمت برمجة المؤشر من الصفر ويعتمد على منطق خاص غير منسوخ من سكربتات مفتوحة المصدر.

--------------------------------------------------------------------------------------------------------------------

🇸🇦 التحديثات – النسخة الجديدة (Abusuhil Bullish Candles)

✅ تم تغيير الملصقات بشكل أوضح: باستخدام دوائر ملونة أسفل الشموع بدلًا من المربعات لتفادي التراكب.

🟦 إضافة جدول تفاعلي على الشارت يعرض أسماء النماذج وألوانها المخصصة.

🎨 إمكانية تغيير ألوان كل نموذج من الإعدادات حسب رغبة المستخدم.

🧩 تفعيل/تعطيل كل نموذج على حدة من خلال إعدادات منفصلة.

🔔 إضافة تنبيه احترافي واحد يتم تفعيله عند تحقق أي نموذج نشط من النماذج المحددة.

📋 توافق كامل مع سياسة TradingView:

لا يحتوي على أكواد منسوخة أو مبنية على مؤشرات داخلية.

لا تكرار للوظائف أو العناوين.

وصف واضح مع تحكم كامل للمستخدم.

🇬🇧 Updates – Latest Version (Abusuhil Bullish Candles)

✅ Clearer Signal Labels: Now uses colored circles under candles instead of labels to avoid overlapping.

🟦 Interactive Table showing pattern names and user-defined colors.

🎨 Customizable colors for each candlestick pattern from the settings menu.

🧩 Toggle each pattern independently using dedicated checkboxes.

🔔 Single professional alert condition that triggers only when any enabled pattern is detected.

📋 Fully compliant with TradingView's publishing policy:

No reused or built-in indicator code.

No duplicated logic or misleading titles.

Clean and modular design with full user customization.

ATR Percentage TableSimple ATR shows the average price change per candle. In order to enter a trade, I need to know how much percent I will win.

I should enter the game for the cross with the highest percentage change. I created a table by entering a cross name in each line in the list and made it possible to follow the changes in the active window.

I sorted the ATR change percentages from largest to smallest. Being able to see the highest percentage change is an answer to the question of which crosses I should choose to open a trade.

Filtered DTR Table📊 Filtered Daily True Range (DTR) Indicator

This indicator calculates and displays a filtered version of the Daily True Range (DTR) over the last 14 trading days, using high and low prices of each day.

It filters out extreme values by excluding any daily range that is:

Less than 0.5× the average range

Greater than 2× the average range

The indicator shows a table in the bottom-right corner of the main chart, containing:

Filtered ATR – The average of valid (filtered) daily ranges over the past 14 days, based on the high-low difference.

Current Day's Range – The high-low range of the current trading day.

% of ATR – How much of the filtered ATR has been covered by today's range, expressed as a whole number percentage.

Trend Table ZeeZeeMonMulti-Timeframe Trend Indicator

Overview

This indicator identifies trends across multiple higher timeframes and displays them in a widget on the right side of the chart. It serves as an alternative trend-filtering tool, helping traders align with the dominant market direction. Unlike traditional moving average-based trend detection (e.g., price above/below a 200 MA), this indicator assesses whether higher timeframes are genuinely trending by analyzing swing highs and lows.

Trend Definition

Uptrend: Higher highs and higher lows.

Downtrend: Lower highs and lower lows.

A trend reversal occurs when a prior high/low is breached (e.g., in a downtrend, breaking the last high signals an uptrend).

Customization Options

Lookback Period: Adjusts the sensitivity for identifying swing highs/lows (pivot points). A shorter lookback detects more frequent pivots.

Historical Pivot Visibility: Toggle to display past swing highs/lows for verification.

Support/Resistance Lines: Show dynamic levels from recent pivots on higher timeframes. Breaching these lines indicates potential trend changes.

Purpose

Helps traders:

Confirm higher timeframe trends before entering trades.

Monitor proximity to trend reversals.

Fine-tune pivot sensitivity for optimal trend detection.

Note: Works best as a supplementary trend filter alongside other trading strategies.

Gap Day Stats TableDescription:

This Pine Script helps you analyze gap up and gap down days using a user-defined gap percentage threshold. It generates a real-time statistics table that tracks:

📈 Number of Gap Up Days

🔻 How many of those days closed lower (Open > Close)

🧮 Total points lost on such gap up days (Open - Close)

📉 Number of Gap Down Days

🔺 How many of those days closed higher (Close > Open)

🧮 Total points gained on such gap down days (Close - Open)

🔧 Customization:

Gap threshold is adjustable via input

Automatically updates stats daily

Ideal for spotting behavioral edge in gaps

This tool is useful for traders building gap trading systems, mean reversion models, or studying post-gap behavior in equities and indices.

ATR Table with Average [filatovlx]ATR indicator with advanced analytics

Description:

The ATR (Average True Range) indicator is a powerful tool for analyzing market volatility. Our indicator not only calculates the classic ATR, but also provides additional metrics that will help traders make more informed decisions. The indicator displays key values in a convenient table, which makes it ideal for trading in any market: stocks, forex, cryptocurrencies and others.

Main functions:

Current ATR value:

Current ATR (Points) — the current ATR value in points. It shows the absolute level of volatility.

Current ATR (%) — the current ATR value as a percentage of the price. It helps to estimate the volatility relative to the current price of an asset.

The ATR value on the previous bar:

ATR 1 Bar Ago (Points) — the ATR value on the previous bar in points. Allows you to compare the current volatility with the previous one.

ATR 1 Bar Ago (%) — the ATR value on the previous bar as a percentage. It is convenient for analyzing changes in volatility

Индикатор ATR с расширенной аналитикой

Описание:

Индикатор ATR (Average True Range) — это мощный инструмент для анализа волатильности рынка. Наш индикатор не только рассчитывает классический ATR, но и предоставляет дополнительные метрики, которые помогут трейдерам принимать более обоснованные решения. Индикатор отображает ключевые значения в удобной таблице, что делает его идеальным для использования в торговле на любых рынках: акции, форекс, криптовалюты и другие.

Основные функции:

Текущее значение ATR:

Current ATR (Points) — текущее значение ATR в пунктах. Показывает абсолютный уровень волатильности.

Current ATR (%) — текущее значение ATR в процентах от цены. Помогает оценить волатильность относительно текущей цены актива.

Значение ATR на предыдущем баре:

ATR 1 Bar Ago (Points) — значение ATR на предыдущем баре в пунктах. Позволяет сравнить текущую волатильность с предыдущей.

ATR 1 Bar Ago (%) — значение ATR на предыдущем баре в процентах. Удобно для анализа изменения волатильности.

Среднее значение ATR за последние 5 баров:

ATR Avg (5 Bars) (Points) — среднее значение ATR за последние 5 баров в пунктах. Показывает сглаженный уровень волатильности.

ATR Avg (5 Bars) (%) — среднее значение ATR за последние 5 баров в процентах. Помогает оценить общий тренд волатильности.

Преимущества индикатора:

Удобство использования: Все ключевые значения выводятся в компактной таблице, что экономит время на анализ.

Гибкость: Возможность настройки периода ATR и длины скользящего среднего под ваши торговые стратегии.

Универсальность: Подходит для любых рынков и таймфреймов.

Наглядность: Процентные значения ATR помогают быстро оценить уровень волатильности относительно цены актива.

Повышение точности: Дополнительные метрики (например, среднее значение ATR) позволяют лучше понимать текущую рыночную ситуацию.

Для кого этот индикатор?

Трейдеры, которые хотят лучше понимать волатильность рынка.

Скальперы и внутридневные трейдеры, которым важно быстро оценивать изменения волатильности.

Инвесторы, которые используют ATR для определения стоп-лоссов и тейк-профитов.

Разработчики торговых стратегий, которым нужны точные данные для тестирования и оптимизации.

Как это работает?

Индикатор автоматически рассчитывает все значения и выводит их в таблицу на графике. Вам не нужно вручную считать или анализировать данные — просто добавьте индикатор на график, и вся информация будет перед вами.

Timeframe Display Table with CustomizationsPlaces a single cell table in the top right of the chart to display the currently viewed timeframe at all times on the chart.

Custom Trend TableManual input of trend starting with Daily Time frame, then H4 and H1.

If Daily and H4 are the same trend we can ignore H1 trend (N/A).

M15 Buy or Sell comes automatically depending on what the higher time frame trends are.

If Daily and H4 are bearish, then we look for Selling opportunities on M15.

If Daily and H4 are bullish, then we look for Buying opportunities on M15.

If Daily and H4 are different trends, then H1 trend will determine M15 Buy or Sell.

Works for up to 4 pairs / Symbols. If you need more, just add the indicator twice and on the second settings, move the placement of the table to a different location (Eg: Top, Middle) so you can see up to 8 Symbols. Repeat this process if required.

UM VIX status table and Roll Yield with EMA

Description :

This oscillator indicator gives you a quick snapshot of VIX, VIX futures prices, and the related VIX roll yield at a glance. When the roll yield is greater than 0, The front-month VX1 future contract is less than the next-month VX2 contract. This is called Contango and is typical for the majority of the time. If the roll yield falls below zero. This is considered backwardation where the front-month VX1 contract is higher than the value of the next-month VX2 contract. Contango is most common. When Backwardation occurs, there is usually high volatility present.

Features :

The red and green fill indicate the current roll yield with the gray line being zero.

An Exponential moving average is overlaid on the roll yield. It is red when trending down and green when trending up. If you right-click the indicator, you can set alerts for roll yield EMA color transitions green to red or red to green.

Suggested uses:

The author suggests a one hour chart using the 55 period EMA with a 60 minute setting in the indicator. This gives you a visual idea of whether the roll yield is rising or falling. The roll yield will often change directions at market turning points. For example if the roll yield EMA changes from red to green, this indicates a rising roll yield and volatility is subsiding. This could be considered bullish. If the roll yield begins falling, this indicates volatility is rising. This may be negative for stocks and indexes.

I look for short volatility positions (SVIX) when the roll yield is rising. I look for long volatility positions (VXX, UVXY, UVIX) when the roll yield begins falling. The indicator can be added to any chart. I suggest using the VX1, SPY, VIX, or other major stock index.

Set the time frame to your trading style. The default is 60 minutes. Note, the timeframe of the indicator does NOT utilize the current chart timeframe, it must be set to the desired timeframe. I manually input text on the chart indicator for understanding periods of Long and Short Volatility.

Settings and Defaults

The EMA is set to 55 by default and the table location is set to the lower right. The default time frame is 60 minutes. These features are all user configurable.

Other considerations

Sometimes the Tradingview data when a VX contract expires and another contract begins, may not transition cleanly and appear as a break on the chart. Tradingview is working on this as stated from my last request. This VX contract from one expiring contract to the next can be fixed on the price chart manually: ( Chart settings, Symbol, check the "Adjust for contract changes" box)

Observations

Pull up a one-hour chart of VX1 or SPY. Add this indicator. roll it back in time to see how the market and volatility reacts when the EMA changes from red to green and green to red. Adjust the EMA to your trading style and time frame. Use this for added confirmation of your long and short volatility trades with the Volatility ETFs SVIX, SVXY, VXX, UVXY, UVIX. or use it for long/short indexes such as SPY.